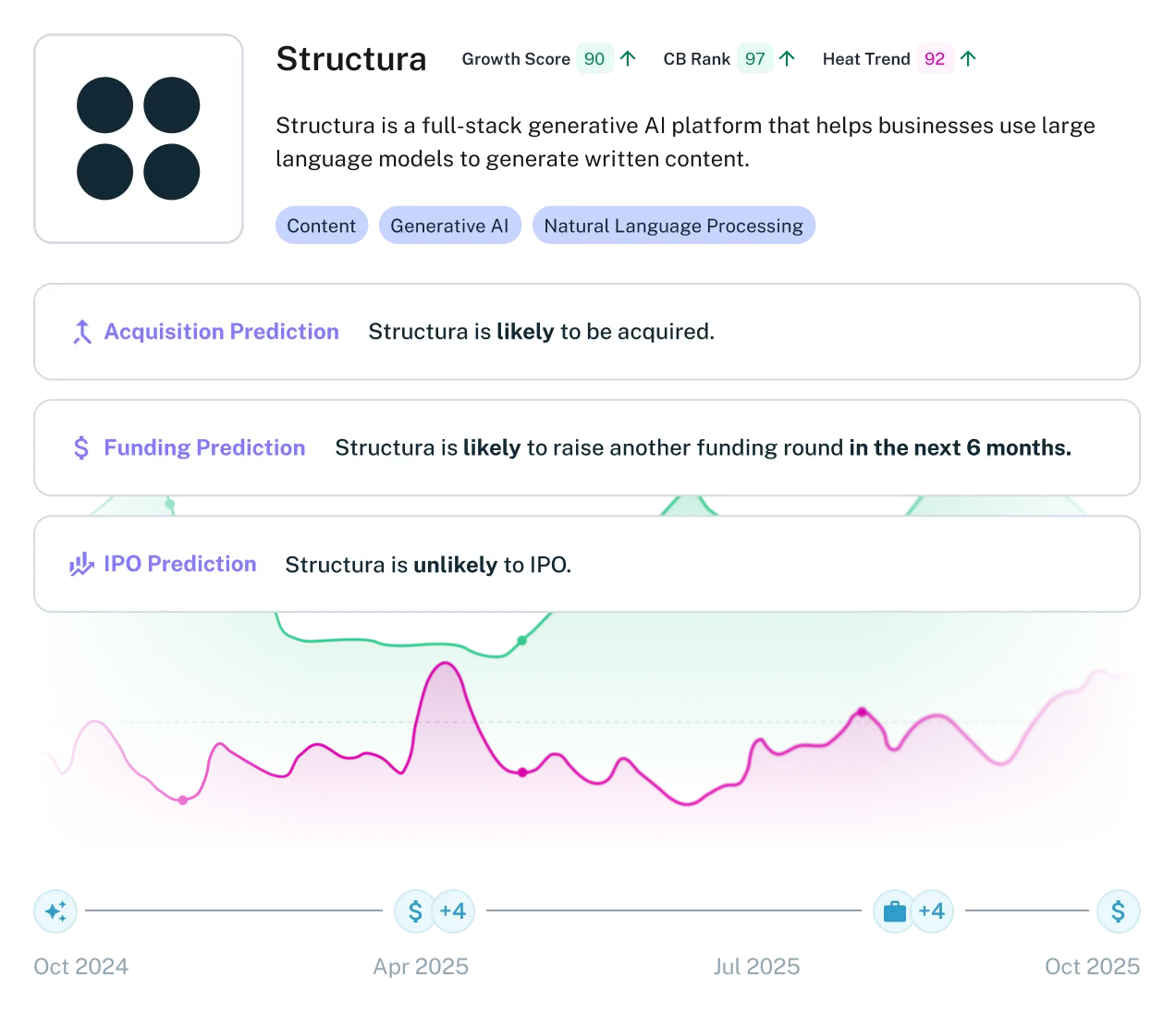

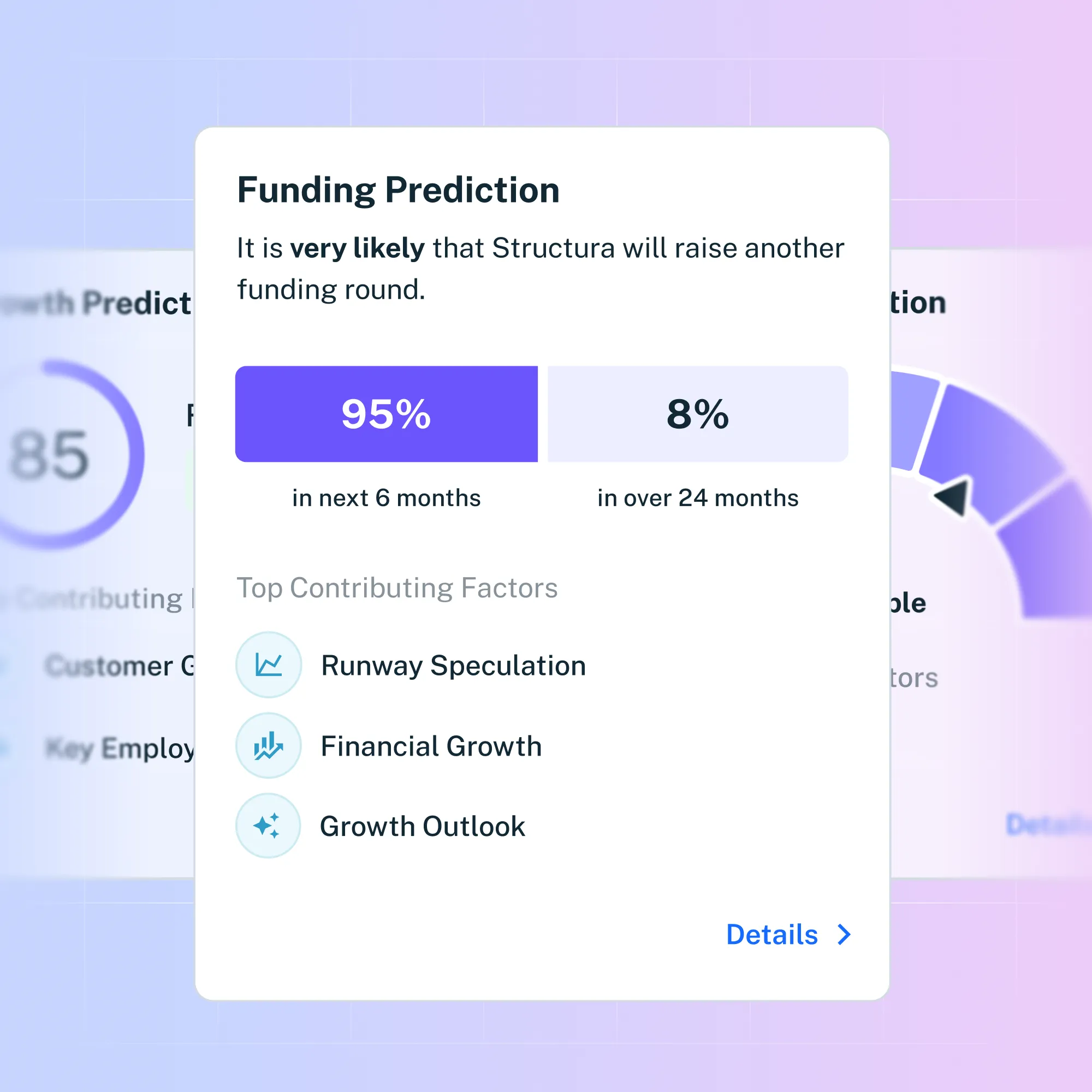

Meet the new Crunchbase: AI-powered, predictive company intelligence. We’re moving beyond historical data with predictions about future company activity.

AI in sales is the use of artificial intelligence to simplify, optimize and improve sales processes. Learn how sales automation can drive revenue growth.

Sales intelligence tools offer valuable insights and data to improve the performance of sales teams. Here are the top sales intelligence platforms and software.

Rebecca Strehlow

,

Copywriter at Crunchbase

at

Win in the Private Market

Spot companies about to grow, fundraise, or exit with predictive intelligence.

.svg)

.webp)

.webp)

.webp)