As the global health crisis of 2020 continues to play out, there have been many comparisons with the economic events of 2008. When the first wave of the pandemic hit and the stock markets crashed in March, another global financial crisis seemed inevitable. So founders will have to be forgiven for assuming their chances of getting funding in 2020 were nixed.

But events haven’t entirely played out the way we expected. Subsequent to the March crash, stock markets made an almost complete recovery. Tech stocks were among the biggest drivers for this resurgence, given the sudden shift to remote working and increased dependence on online connectivity.

However, it’s not just publicly traded companies that have remained unexpectedly buoyant. Now that we’re well into the pandemic and have enough data to perform a meaningful analysis, I thought it would be interesting to look at some of the trends in funding mapped against events in the stock markets: both in 2020 and in 2008. I reached out to my friends at Sisense for some data help, and together we were able to put together some interesting analysis.

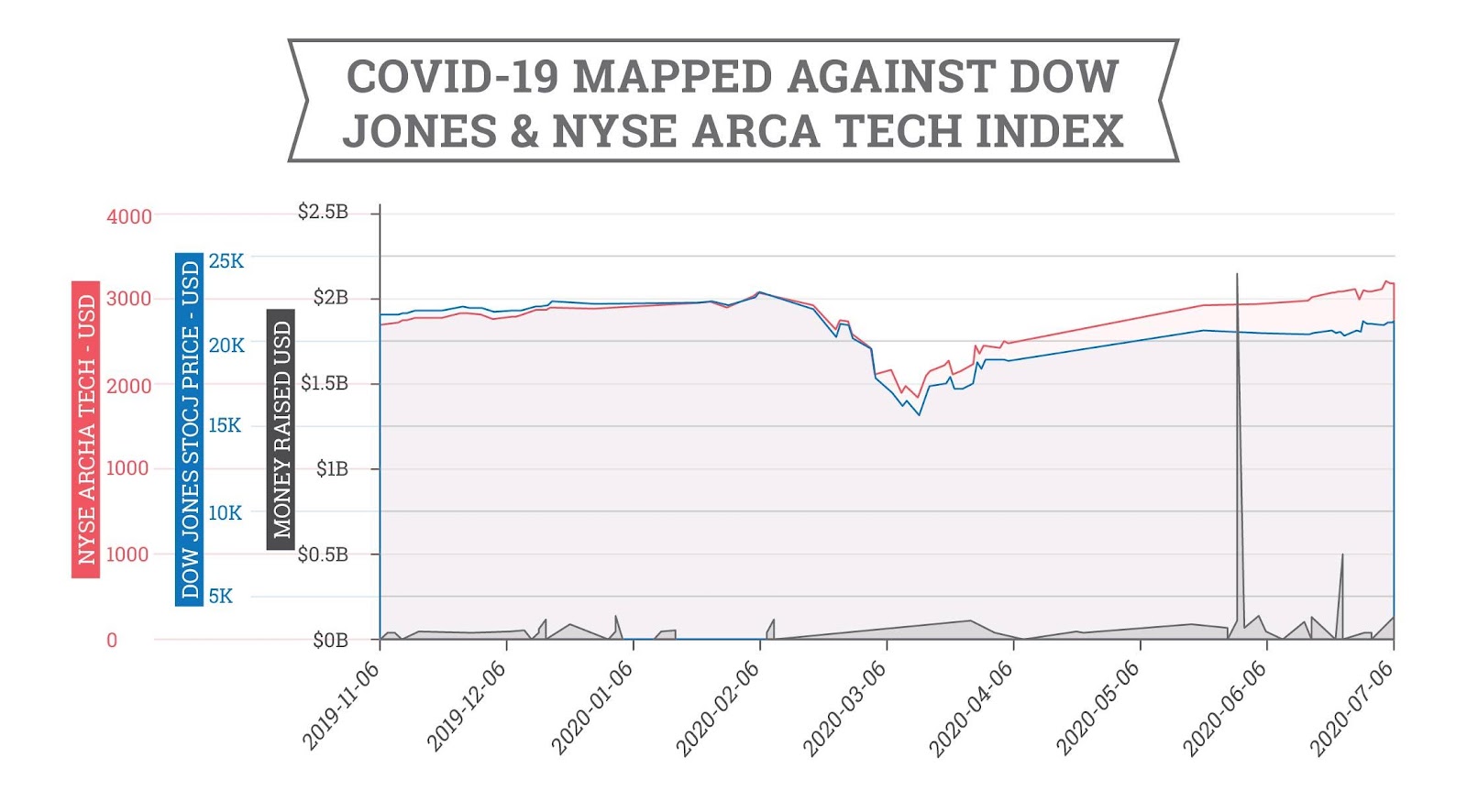

To start, data from Crunchbase shows that the total value of venture funding increased in the months following the shock of the pandemic taking hold in March. In fact, it increased dramatically in the third quarter, corresponding with the increasing number of funding rounds.

Interestingly, the data shows a clear anomaly on March 23, caused by two especially large funding rounds within two days of the stock market crash’s lowest valley. One of these rounds was for CureFit, an Indian fitness club chain–it’s important to remember here that India was hit later in the pandemic. The other was an unknown series for iCapital Network, which had likely been in progress before the virus took hold, as the fintech startup’s round involved multiple international banking concerns.

In any event, it’s worth noting that funding trends have been known to lag behind the stock market due to the lead times involved in organizing a funding round.

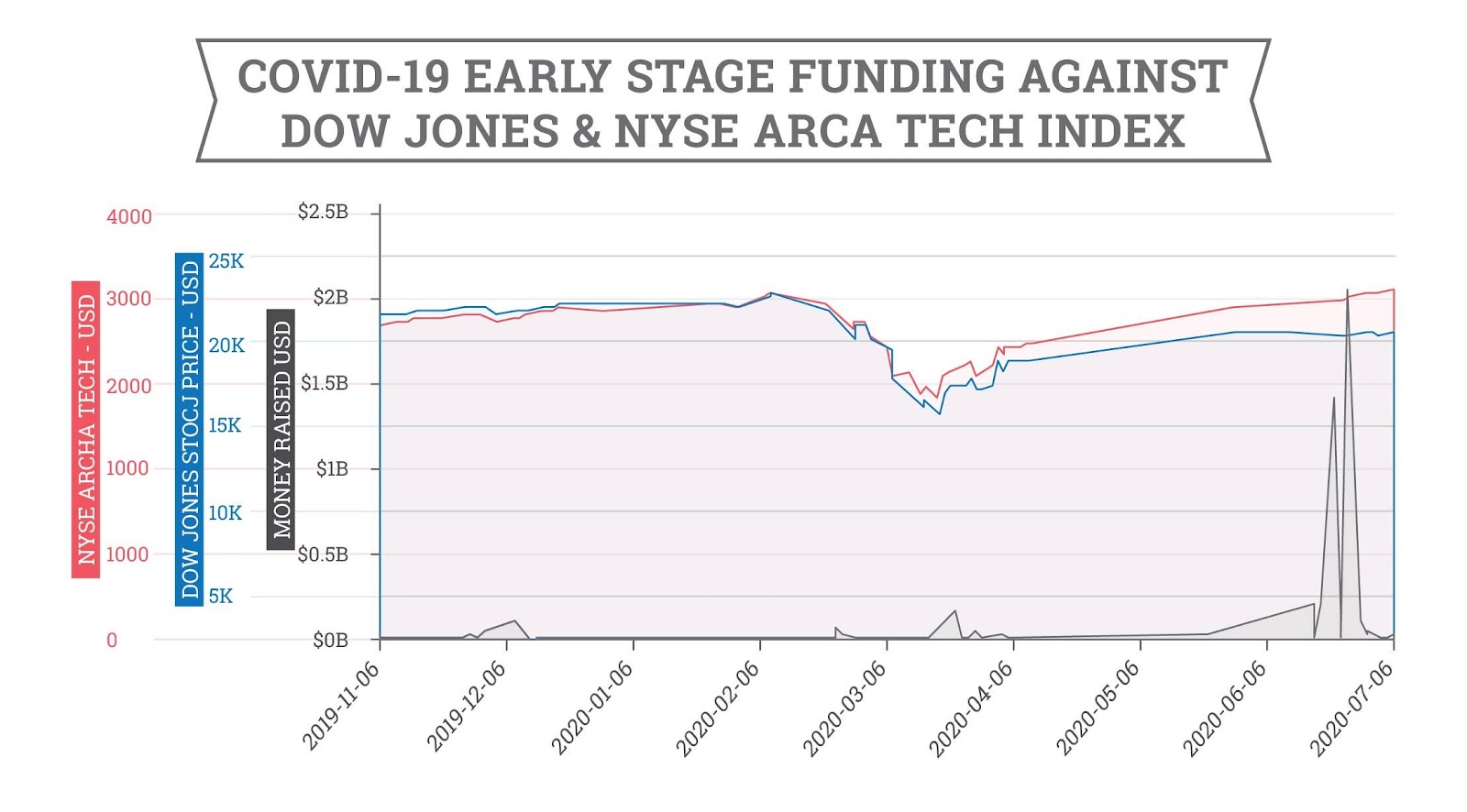

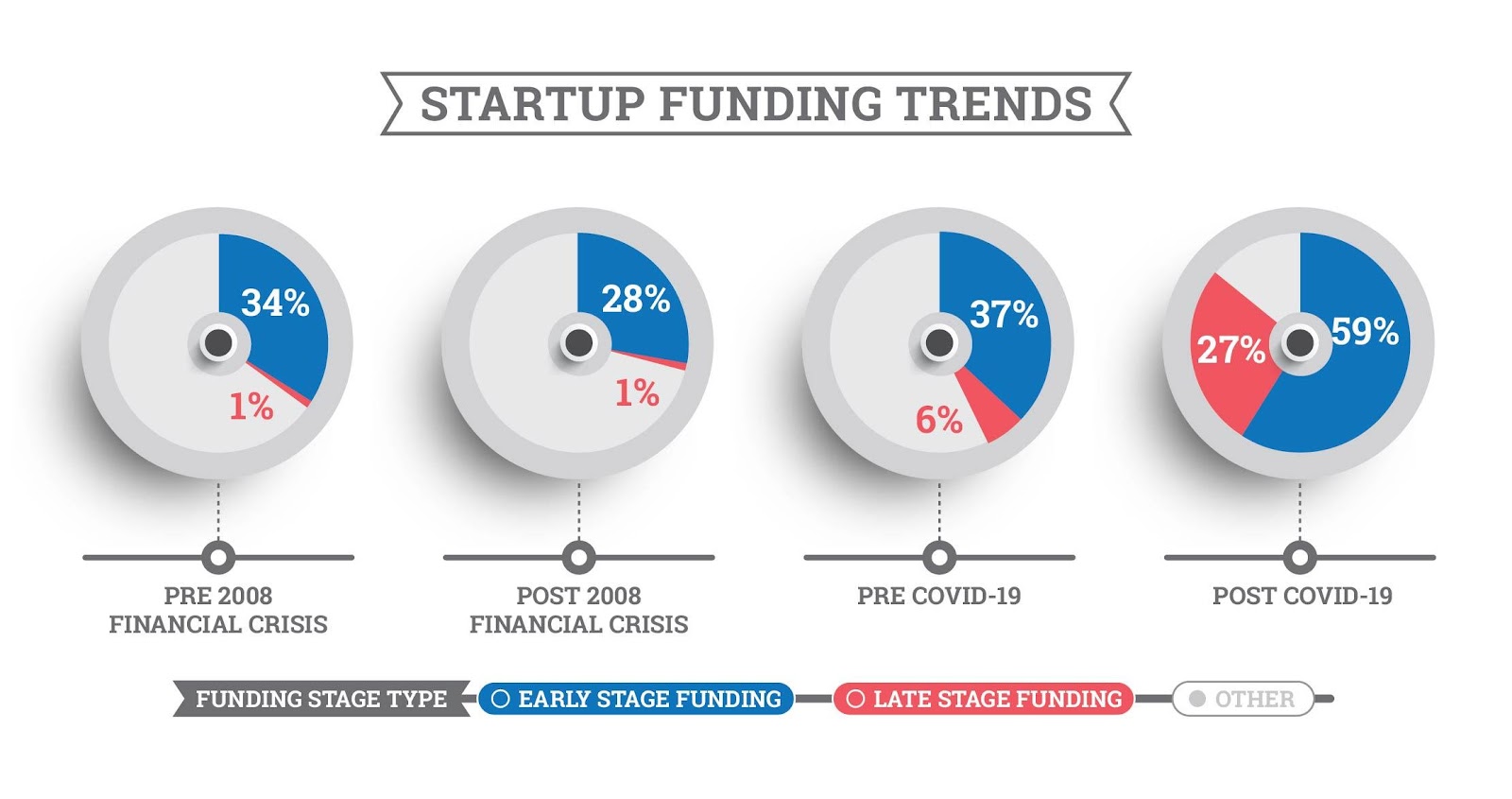

Perhaps even more intriguingly, the peak that we can see toward the end of July was almost all attributable to early-stage funding, which was clearly visible when I drilled down into the types of funding.

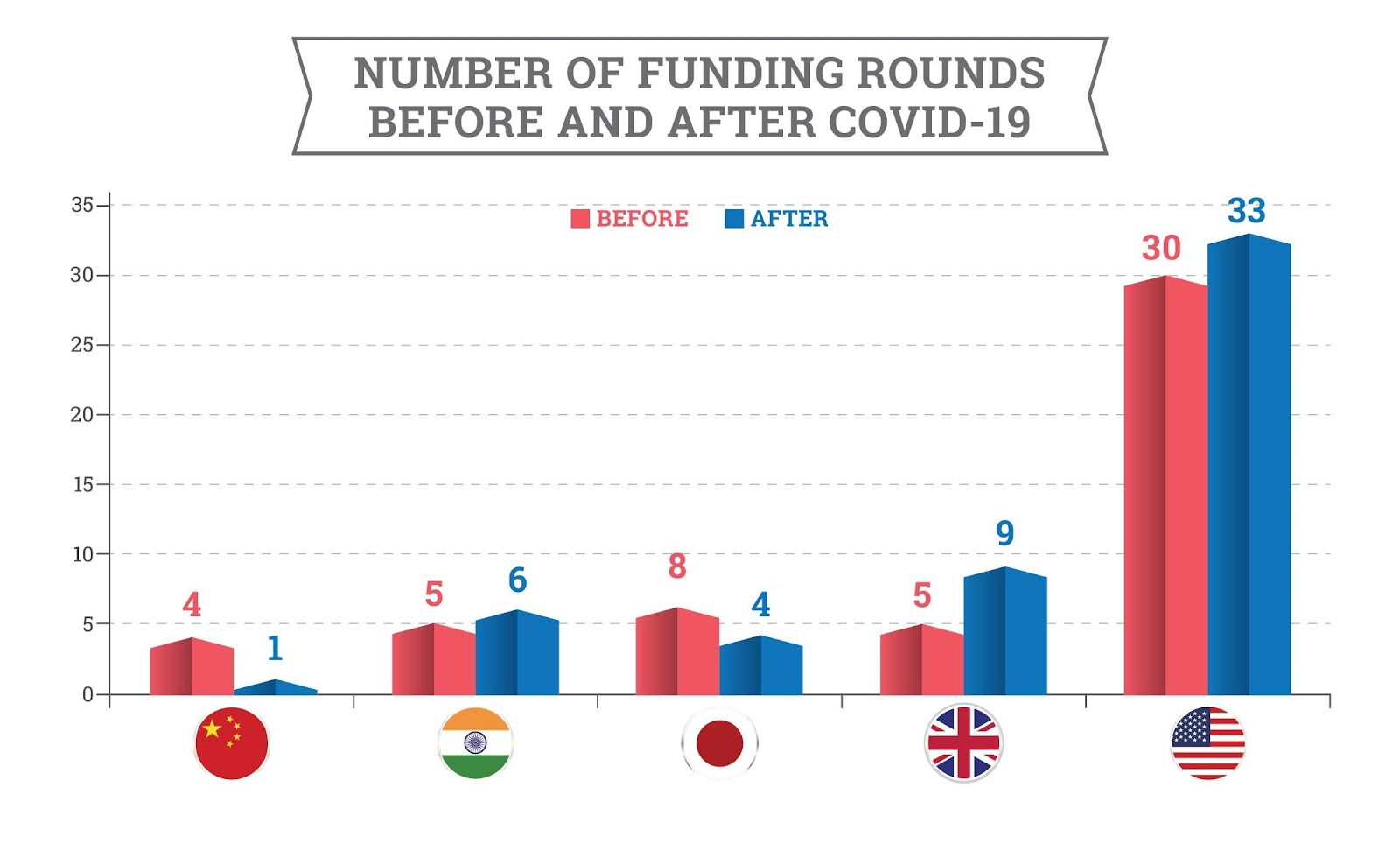

Although the U.S. emerged as one of the most heavily impacted countries relatively early on in the pandemic, over half of all funding rounds took place in the states. The U.K. is a distant second with only 11 percent of the rounds raised during this period.

Comparing to 2008

To create a methodology for comparing events of 2020 with those in 2008, I looked across major stock indices and determined the lowest price during the event to be the “middle” of the period under scrutiny.

For the 2008 crisis, this lowest point took place on March 9, 2009, a few months after the headlines about Lehman Brothers going bankrupt. For the coronavirus, the lowest point took place on March 24, 2020, less than two weeks after President Trump announced a European travel ban.

To look at what happened in venture funding before and after each low point, I collected and analyzed 20 weeks worth of data from Crunchbase for each of the four relevant time frames.

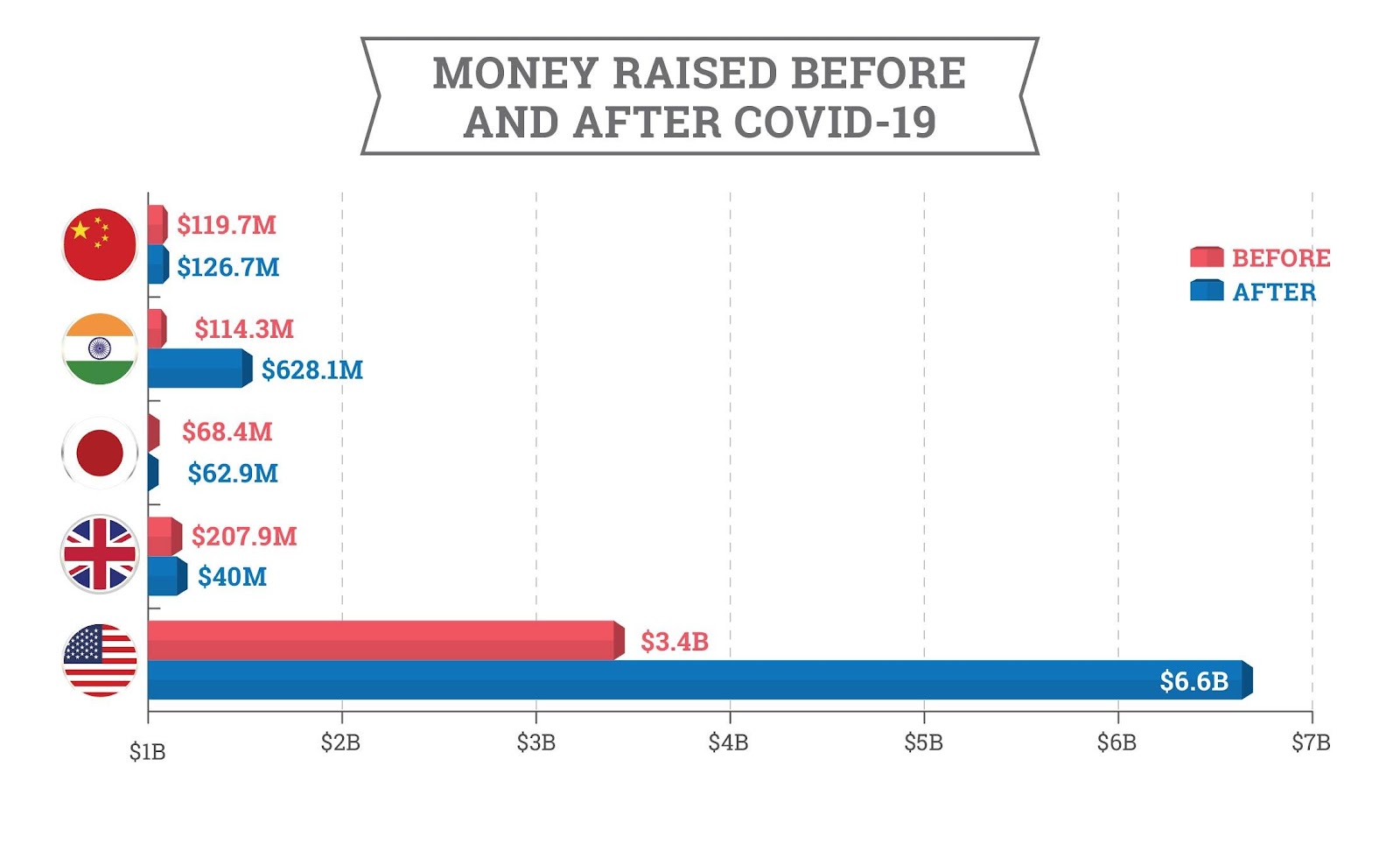

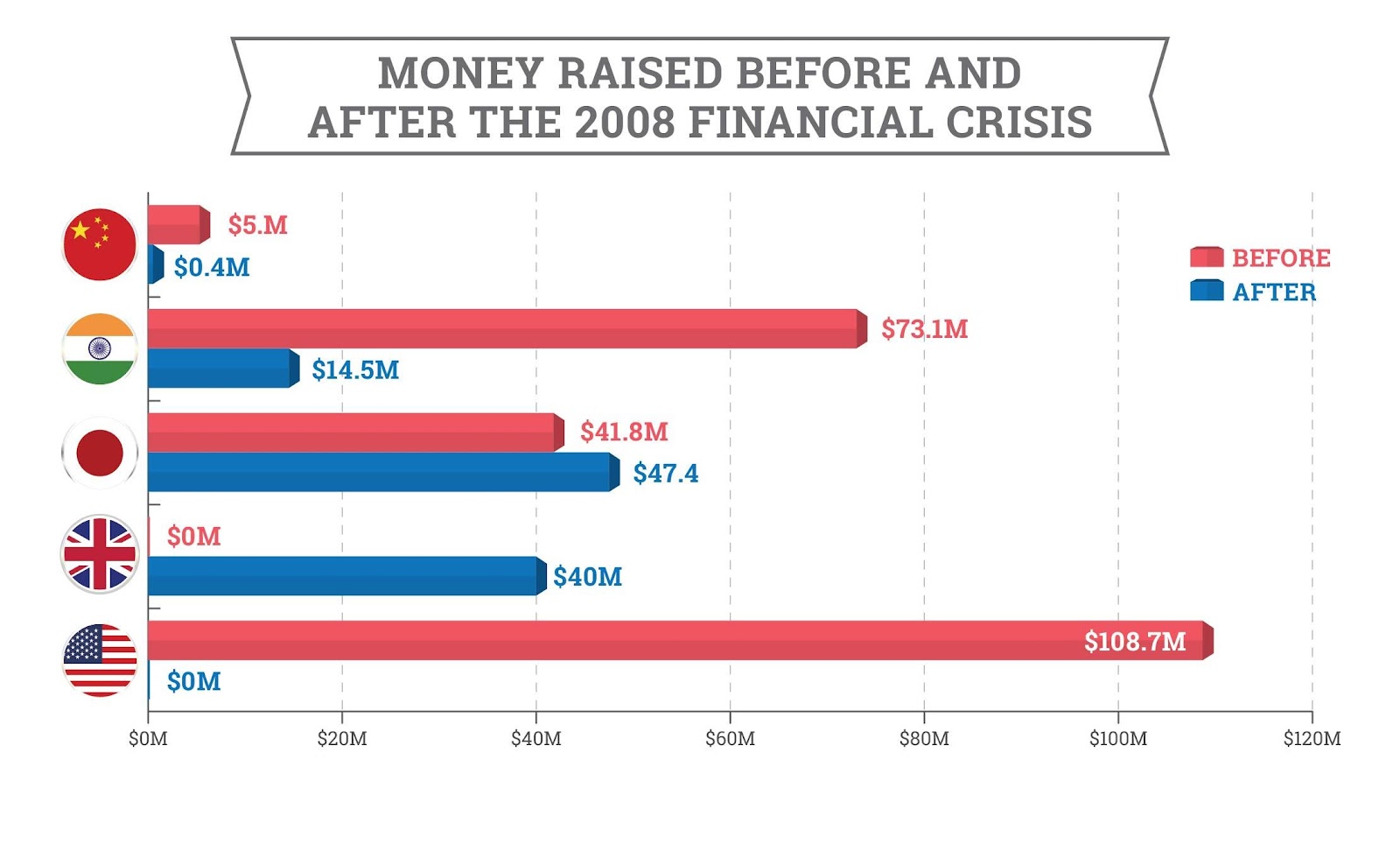

Looking at activity during those specific time frames, it’s evident that investor confidence in startups rebounded far more quickly and sharply in 2020 than it did in 2008-09. Particularly in the U.S., the total money raised and the number of funding rounds increased dramatically in the months after the first wave of the pandemic. In all of the top five countries, funding either remained stable or increased.

In 2008, the overall trend was that confidence in funding dropped off considerably, with the most pronounced changes in the U.S. and China. The U.K. appears to be an anomaly caused by missing round size figures, but comparing the funding rounds shows that there was only one either side of the 2008 crash, which distorts the charts.

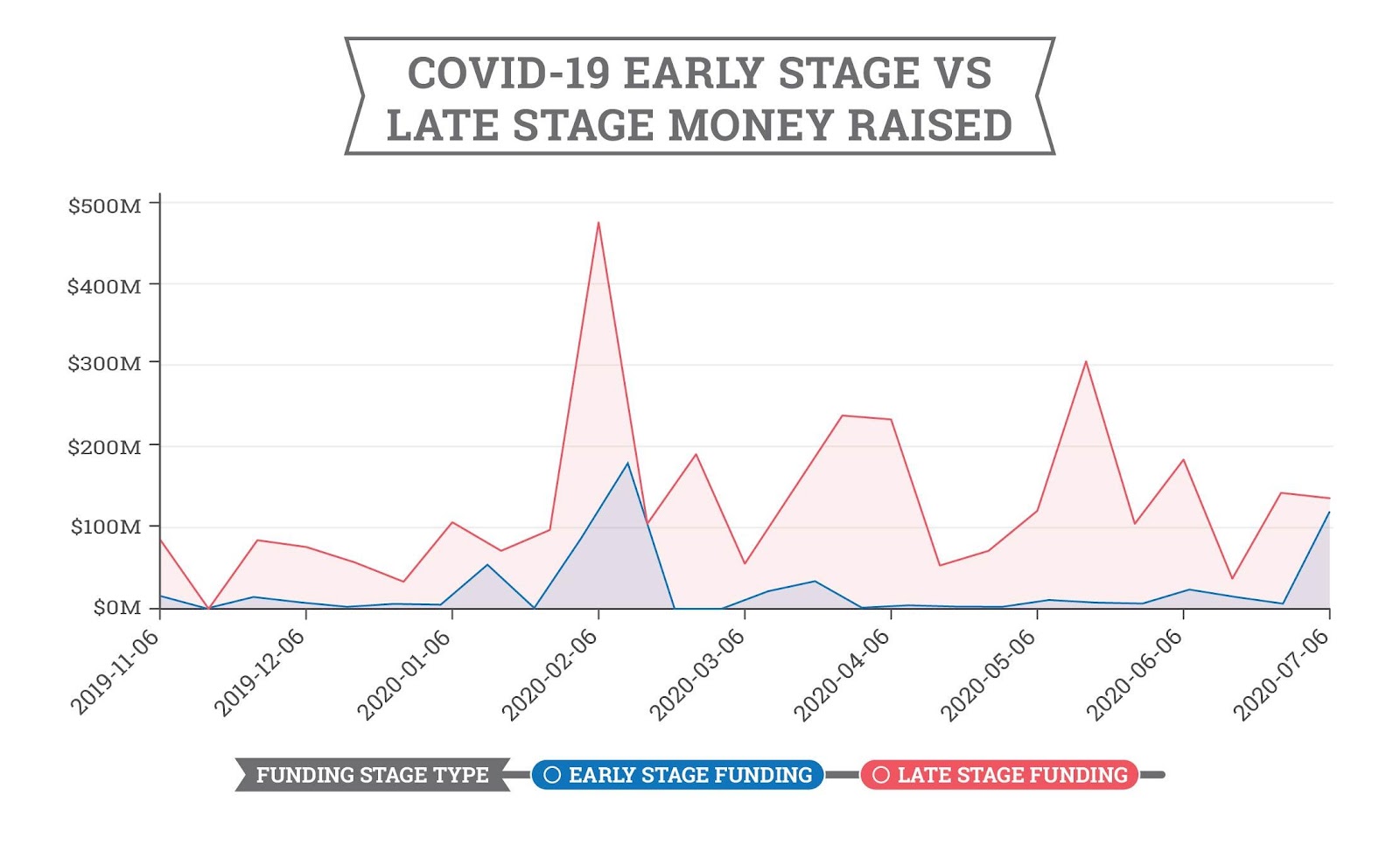

Contrasting the type of funding shows that not only did the recovery take place on different schedules, there were other differences at play as well. In 2008, funding was concentrated on early-stage investment both before and after the crash. However, in 2020, investors showed more of an appetite for late-stage funding in the months immediately following the March meltdown.

Nevertheless, as the first pandemic wave appeared to subside, we can see from the chart above that early-stage investment made a startling resurgence over the late stage during the third quarter of 2020.

The Crunchbase Q3 Global Venture Report also shows that overall, funding is holding up remarkably better than expected in 2020.

Digging deeper

One noticeable difference between 2008 and 2020 is the exponential growth of the markets. The charts above show U.S. funding at around $100 million post-2008 crisis, whereas it’s now up to $7 billion, mainly reflecting the expansion of the technology markets over the last decade.

A critical difference, however, is in the type of issue facing the world economy in 2020. The 2008 global financial crisis was precisely that: a financial crisis. It was precipitated by the crash of banks, including Lehman Brothers and Northern Rock, meaning investors were less willing to part with liquid assets.

The exact manner in which the economic impact of the pandemic would pan out was a complete unknown during the early months of 2020. Nevertheless, this is a different kind of crisis, and three quarters into it, we have at least some idea of what it means for the economy. Some sectors, including travel, tourism and hospitality, are obvious casualties, which is likely to continue while the pandemic is ongoing.

However, other sectors have thrived over recent months, giving investors and startups alike an idea of where it’s worthwhile concentrating their time and money. As previously reported by Crunchbase News, online education and software-as-a-service companies lead the pack of new unicorns this year. Life sciences, including biotech and digital health, are currently seeing record investment, both in value and funding rounds.

Generating a new era of innovation

As investors at Greycroft previously told Crunchbase, the pandemic is throwing up new opportunities, perhaps explaining the trend toward early-stage investment.

Startups are innovating on demand for markets including fintech, e-commerce and food and grocery delivery. According to Statista, app downloads for the latter have grown by over 200 percent this year.

Elsewhere, investors are also looking out for startups developing apps that will contribute to a more collaborative and connected remote workplace of the future. Even in this crowded space, genuine innovation is attracting significant funding. For example, MURAL, which is developing a digital workspace for visual thinking, closed a Series B round worth $118 million this summer.

These trends underscore that out of every big crisis comes opportunity. The events of 2008 resulted in some of today’s household names, including Airbnb and Uber. The impact of the pandemic has been even more far-reaching than the last financial crisis. If necessity is truly the mother of invention, then the need to adapt to the changes forced by the pandemic creates a compelling drive for innovation.

None of this is to say that late-stage companies need to go back to the drawing board. After IPOs were said to have hit “bubble” levels in 2019, shares are surprisingly up 60 percent this year, making 2020 the biggest year since Alibaba went public in 2014. As of September, 117 companies had gone public this year.

What’s the outlook?

In light of the unprecedented nature of the pandemic, comparisons with 2008 probably aren’t helpful. However, general stock market trends indicate that investors can expect a strong fourth-quarter performance. Given the tendency for startup funding to lag behind the stock markets, if there are to be any seismic changes to the current status quo, they’re unlikely to happen before 2021.

We now know that surviving the coronavirus pandemic is going to be a marathon, not a sprint, so it’s fair to say that uncertainty will continue into the year ahead. Nevertheless, companies in those sectors proven to weather and thrive through COVID that have made it this far should have no reason to believe they can’t last the distance, all else being equal.

Innovators who can develop solutions that will help individuals and companies overcome the pandemic’s challenges have no reason to hesitate to bring them to the fore as we move into 2021.

As the pandemic continues to spread across the globe, it seems likely that those sectors already negatively impacted will struggle to recover. We can expect these industrywide trends to play out across stocks and VC funding in a comparable way.

Pini Raviv is a software engineer and data scientist with experience as a front-end team leader for an Israeli startup.