The SaaS M&A Report for Q2 2018

4 min read

.svg)

This article will cover the Software Equity Group’s SaaS M&A Snapshot for Q2 for SaaS companies.

We recently got Software Equity Group’s SaaS M&A Snapshot for Q2. SEG is a boutique investment bank focused on M&A for SaaS companies and they put out fantastic data every quarter on what they’re seeing in the market.

They close 8 to 10 deals per year with transactions ranging in size from $15 million to $100’s of millions. Key observations from Q2’s report is as follows:

Deal volume is still high. Transaction volume remains at record highs through 2018 and is tracking 11% higher than 2017.

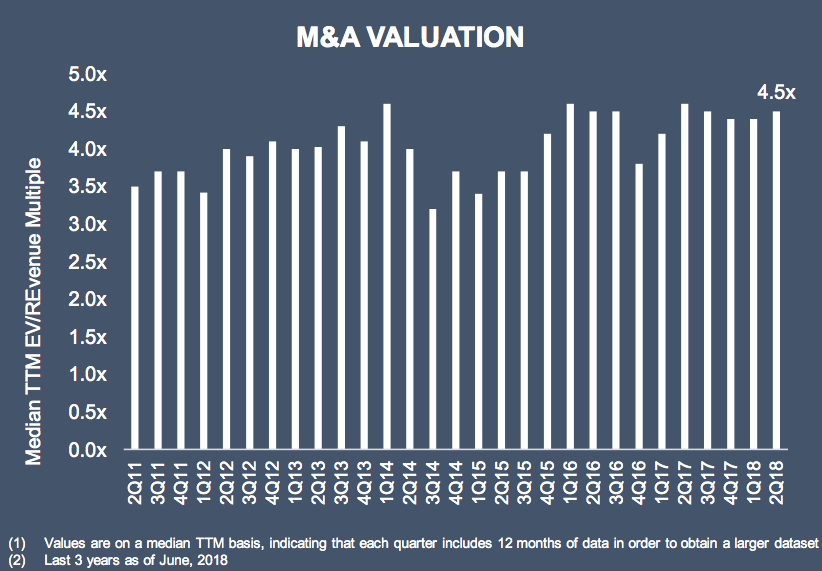

Multiples are good. The median revenue multiple is 4.5x. The median has remained above 4x since 2016 except for Q4 2016 when it dipped to 3.8x. “Consistent with past quarters, approximately one-third of SaaS targets were acquired for 3.0x or less. Meanwhile, approximately one-third of targets were acquired between 3.0x and 6.0x, and the remaining balance was valued at 6.0x or greater.”

If you’re a top performing company with at least $3mm of annual revenue, you can expect to trade for 4x to 5x. In rare cases where an acquirer has to have you and you can afford to walk away from the deal, you may be able to do 8x to 10x, but that’s truly a unique situation.

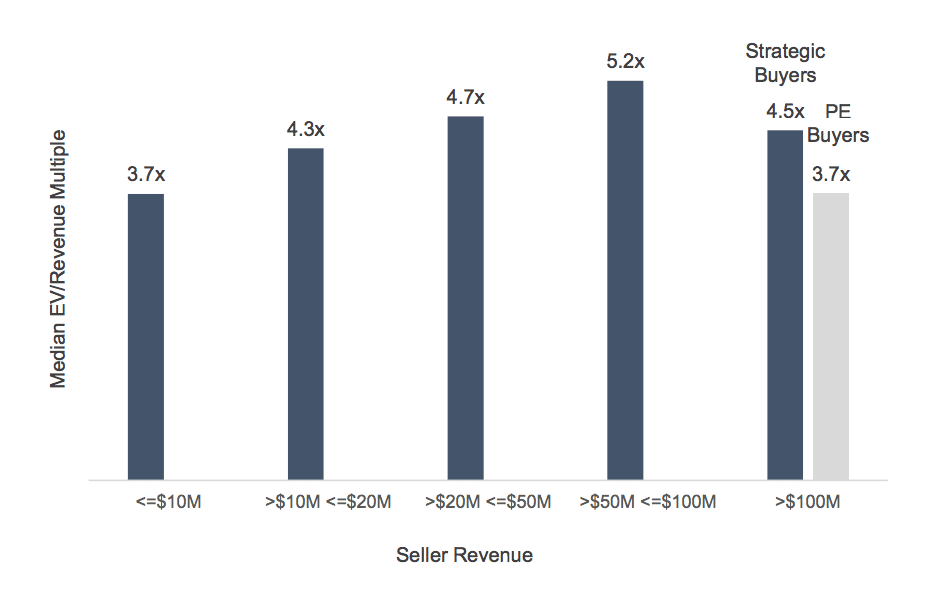

Size drives multiples. “Valuations are largely driven by company size. Organizations exhibiting scale are generally rewarded with higher multiples. Over the past 3 years, companies with revenue between $50M-$100M posted the highest median multiple (5.2x EV/Revenue). 40% of SaaS companies target had 50 employees or less. Nearly 40% had between 50–200 employees and the remaining 20% had greater than 200 employees.” Notably, private equity firms or private equity-backed strategics represent 61% of transactions whereas publicly traded strategics represent the other 39%.

In M&A, companies are valued based off of LTM revenue (last twelve months), not annualized recurring revenue or even forward revenue. SEG tries to push acquirers to apply multiples to these higher revenue figures, but it’s atypical. Depending on how fast you’re growing, there could be a big difference in value between 5x LTM revenue and 5x ARR.

Growth. In order to earn a premium multiple, strive for maintaining at least 40% year over year growth with at least 90% of that revenue coming from contracted recurring streams.

Profitability. If you’re growing under 40% per year or even slower, strive for a 30%+ EBITDA margin. If you’re not profitable, growth needs to be well in excess of 40% to offset. Or you’ve got to be able to make a case that you could be profitable if you wanted to be, but you’re re-investing cash in sales and marketing burning cash in order to spike growth.

Qualitative Factors. Non-financial factors such as the age of the tech, the strength of the team, and the uniqueness of the product all come into play. If your product is good enough, many acquirers will overlook major shortcomings on the financial side.

M&A can take anywhere from 2 months to 2 years depending on what type of process is run (abbreviated versus full) and what the interest level is for your company. When an acquirer solicits you and you say ‘no’, they don’t wait around for you to decide to sell. They either build your tech themselves or they acquire a competitor, even if that competitor isn’t as good as you.

Once either of those two things happens, consider that acquirer gone in the future. We’ve seen this happen first hand when Yahoo tried to acquire one of our portfolio companies. We said ‘no’ believing we could get a higher price later. When we were ready to sell 2 years later, Yahoo no longer a potential acquirer. In those two years, Yahoo had gone out and bought some of our smaller competitors.

Hiring a great banker is critical to maximizing value in an M&A process, and banks like Software Equity Group and Pagemill Partners are ones we like a lot for SaaS companies. If you want an intro, let me know.

Sammy is a co-founder of Blossom Street Ventures. We invest in companies with run rate revenue of $2mm+ and year over year growth of 50%+. We lead or follow in $1mm to $5mm growth rounds and can do inside rounds, secondaries, restructurings, and special situations. We’ve made 16 investments all over the US in SaaS, e-commerce, marketplaces, and low-tech. We can commit in 3 weeks and our check is $1mm. Email Sammy directly at sammy@blossomstreetventures.com.

.webp)

.webp)

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

Unordered list

Bold text

Emphasis

Superscript

Subscript