Relax. There is no other Silicon Valley in sight. That was the headline of last year’s report “Tech Scaleup Silicon Valley” that Mind the Bridge and Crunchbase produced. One year later, we took an updated snapshot of the Bay Area. The headline remains the same, but there is a twist. This year’s headline reads: “Silicon Valley remains the undisputed North Star for both quality and quantity of the innovation throughput of the world.”

Silicon Valley may still be the North Star for quality and quantity, but it isn’t the only place scaleups are thriving. Here are three arguments in favor of continuing to call Silicon Valley the leader in scaleup ecosystems:

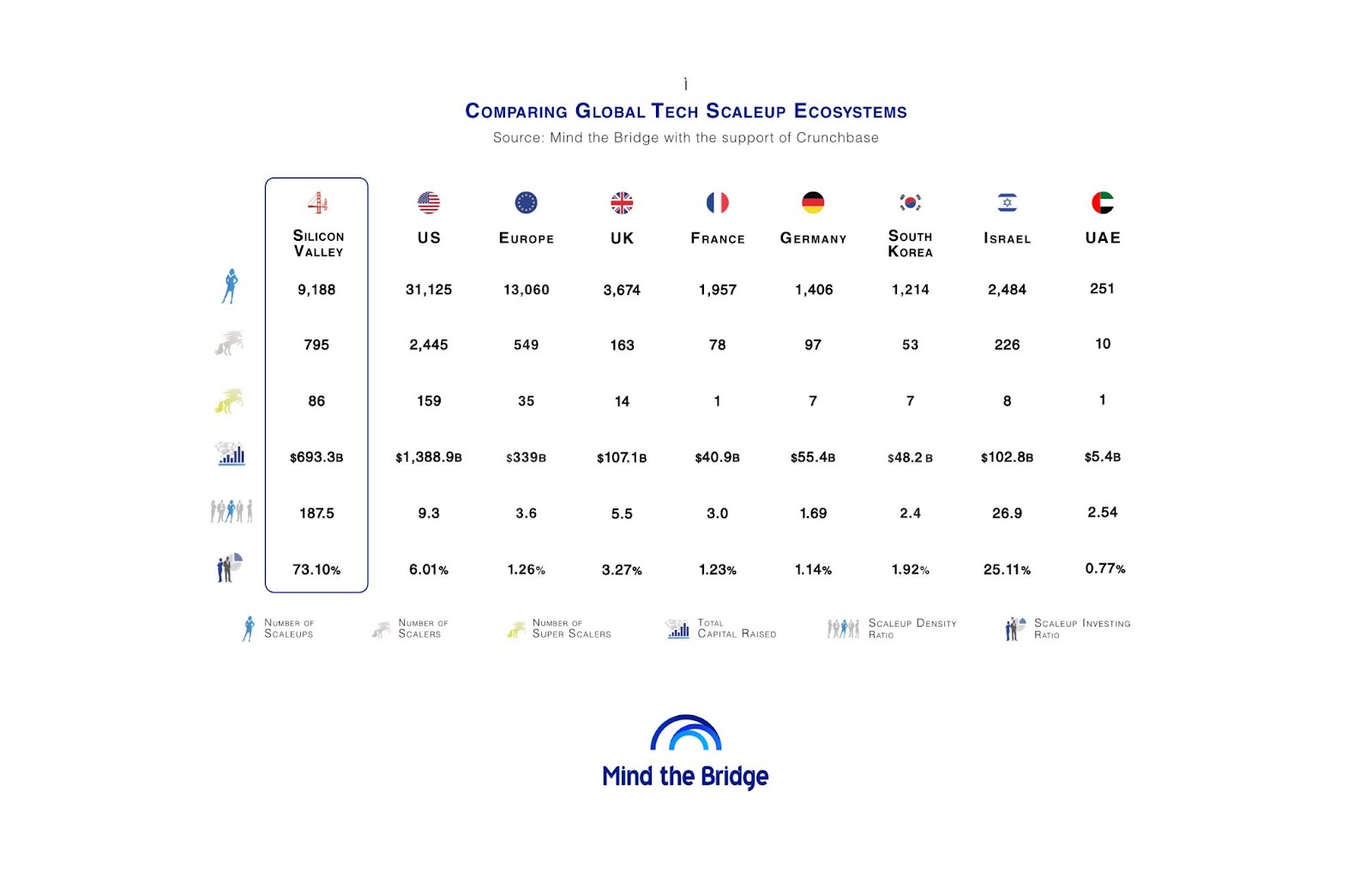

1. It is the hub with the highest density of scaleups and investments in the world, by far

Silicon Valley hosts over 9,000 scaleups. Elsewhere, it takes an entire continent or country such as Europe or China to provide similar figures. Silicon Valley has about 4x more scaleups than Israel (the so-called “Startup Nation”). The gap is even wider in terms of investments. Scaleups headquartered in the Bay Area raised approximately $700 billion in capital to date, which is about half of the total capital made available to U.S. scaleups. This is double the amount raised by their European counterparts and 7x higher than Israel.

2. It is the place with the largest concentration of corporate innovation outposts in the world

According to our latest dedicated study 330 of Fortune 500/Forbes 2000 companies have a dedicated presence in Silicon Valley (many have more than a single outpost). And the trend has accelerated in the past few years, despite COVID-19. For reference, in Israel the corporate innovation contingent is less than half (slightly more than 150 companies).

3. Silicon Valley has become the place to be for government institutions

Government presence in California supporting innovation is a global phenomenon attracting representative institutions from countries, regions, and supranational entities such as the EU.

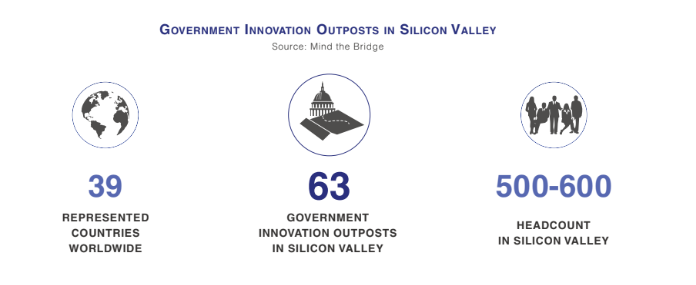

A study we just published tracked 63 active Government Innovation Outposts representing national and regional startup ecosystems from 39 countries. As of 2022, the outposts represent entities from 39 countries worldwide, currently hosting an estimated workforce ranging between 500-600 professionals.

The phenomenon of government institutions setting foot in Silicon Valley is relatively recent and steadily growing. Apart from a few outposts (11, 17% of total) whose presence in Silicon Valley dates back to years before 2000, the vast majority of government institutions have set foot in Silicon Valley in the last two decades, about 60% of which after 2010.

But, there is scaleup life outside of Silicon Valley

The narrative of “the next Silicon Valley” has become outdated. Planners from all over the world trying to replicate the secret sauce of the Bay Area have had limited success. No ecosystem realistically has the possibility to reach the scaleup density levels of the Bay Area.

But today there is a lot of innovation generated outside of the Bay Area that matters. Here are three arguments that highlight how Silicon Valley’s foothold on the title of “leading scaleup ecosytem” may be slipping.

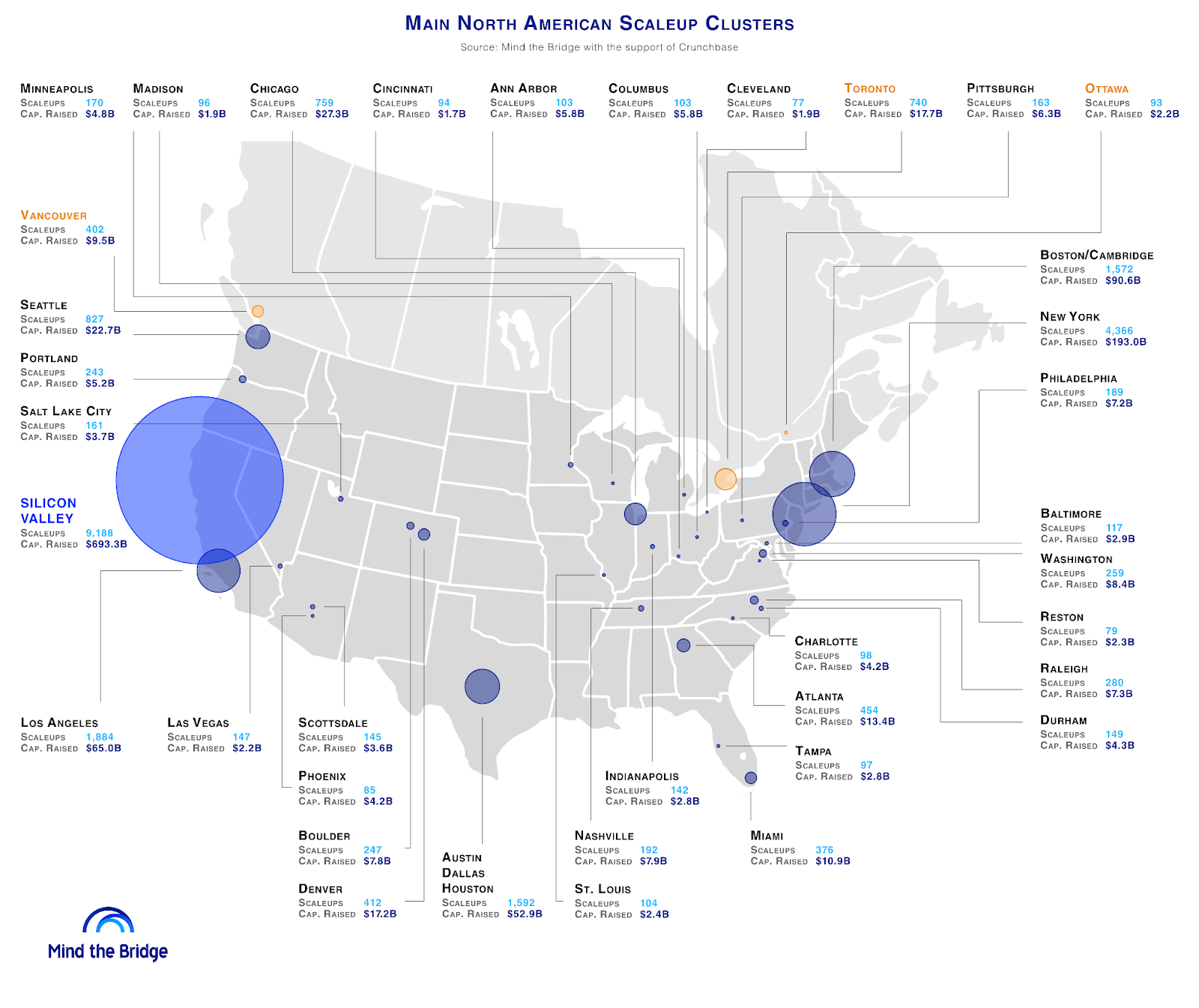

1. In North America alone there are 30-plus clusters able to get beyond critical mass

No single hub is comparable to Silicon Valley. That said, several local ecosystems are experiencing growth.

Not factoring Silicon Valley, we tracked 15 cities across the U.S. and Canada with more than 200 scaleups (that is about the current size of ecosystems such as Amsterdam, Helsinki, Munich, Dublin and Zurich). Twenty-plus other cities have between 100 and 200 scaleups.

This means there is a large pool of innovation scattered across North America that is almost invisible to the companies that focus their scouting activities on ecosystems with larger density.

2. Some U.S. hubs are becoming “Silicon Valley-ish”

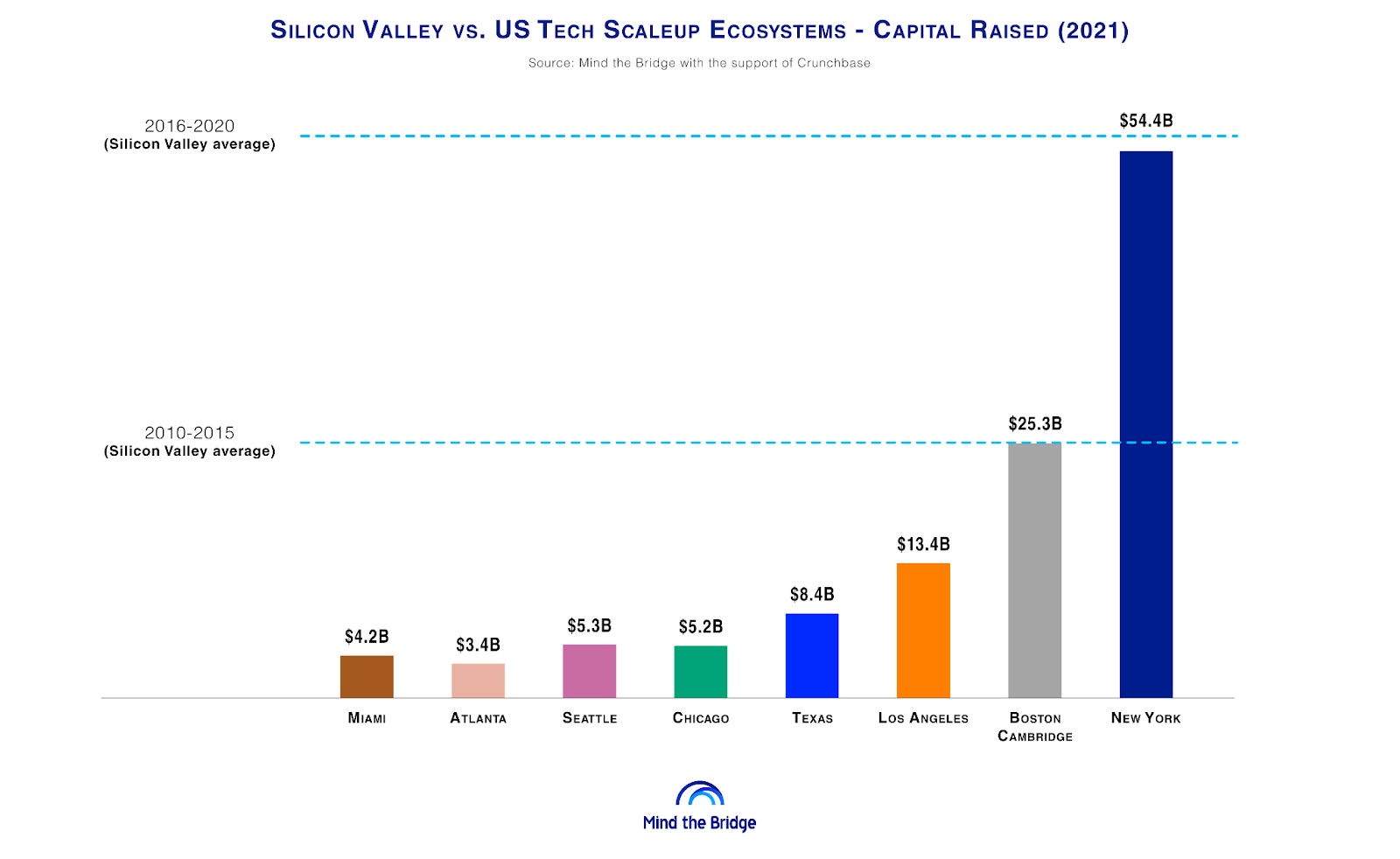

We analyzed and compared nine U.S. hubs showing a significant concentration of scaleup activity: New York, Los Angeles County, Texas (including Austin, Houston and Dallas-Fort Worth), Boston and Cambridge, Seattle, Chicago, Atlanta, and the recently emerging Miami. In the report you can find all the data.

Among them, New York is an emerging comparable (over 4,000 scaleups,–approximately half the number of scaleups in the Bay Area), while Los Angeles, Texas and Boston are approaching being home to 2,000 scaleups each.

In terms of capital raised, New York’s 2021 investments are at the level Silicon Valley was (on average) from 2015-2020, while Boston and Cambridge are closer to capital raised in Silicon Valley from 2010-2015 (an approximately 10-year delay). All other ecosystems researched are raising capital at the level Silicon Valley had in the early years of the new millennium.

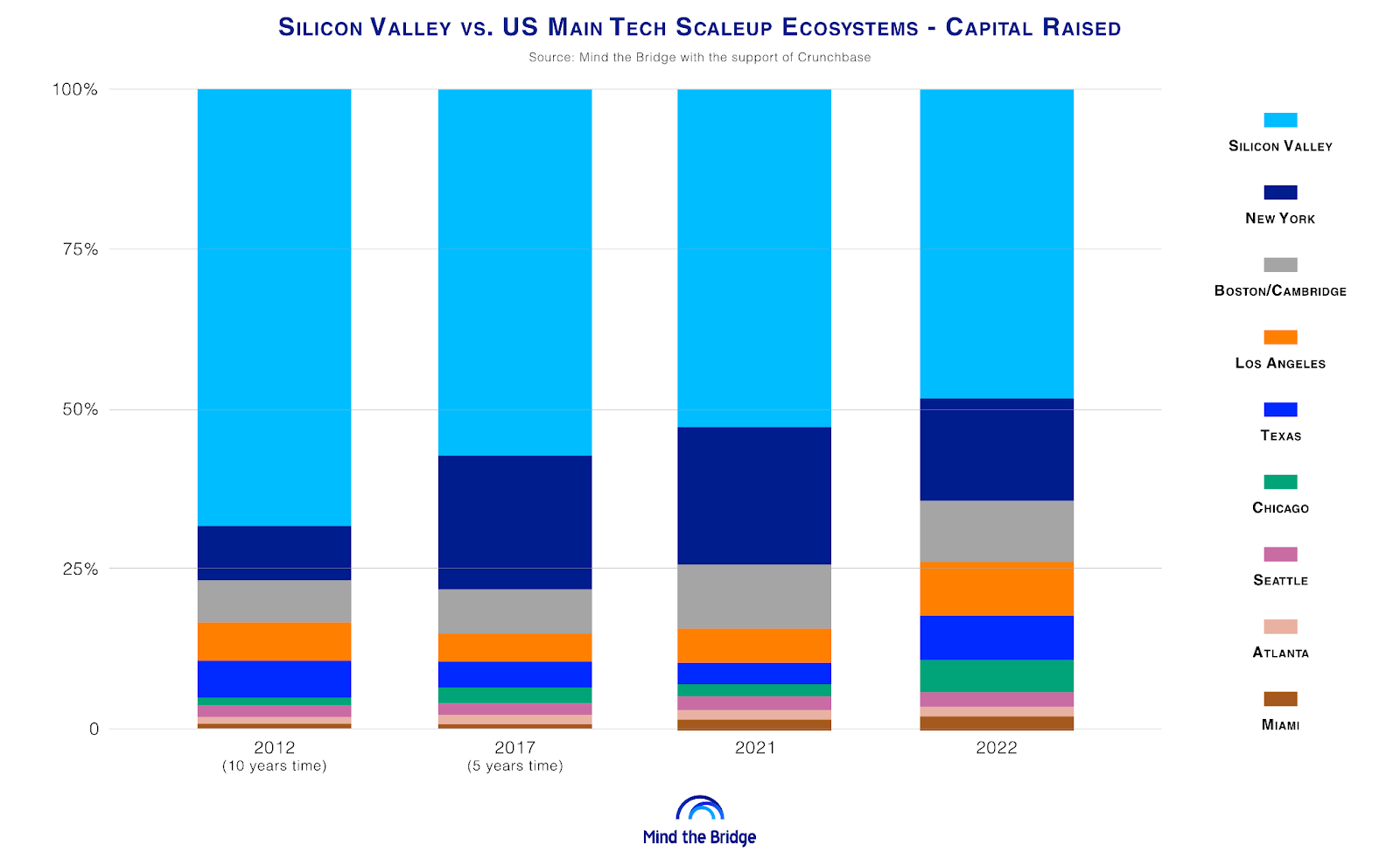

3. From 3:1 to 1:1 in fewer than 10 years

That said, while 10 years ago the scaleups of the eight largest ecosystems were cumulatively raising less than one-third of the amount invested in Silicon Valley, today they have definitely caught up.

Last year, the eight largest scaleup ecosystems outside of Silicon Valley raised $120 billion versus Silicon Valley’s $133 billion. This year, in the first nine months, $64 billion was raised (versus $59 billion in the Bay Area). This could be the beginning of a paradigm shift.

Click here to access the Tech Scaleup Silicon Valley 2022 Report Update.

Alberto Onetti is Chairman of Mind the Bridge.

This article is part of the Crunchbase Community Contributor Series. The author is an expert in their field and we are honored to feature and promote their contribution on the Crunchbase blog.

Please note that the author is not employed by Crunchbase and the opinions expressed in this article do not necessarily reflect official views or opinions of Crunchbase, Inc.