Does Fintech Actually Contribute to Financial Inclusion?

9 min read

.svg)

Accessibility and discrimination have been key themes in the formal financial system since its inception. Recent progressions in technology have allowed fintech to emerge as a way to break down these barriers and positively impact the world through financial inclusion.

The World Bankdefines financial inclusion as having “access to useful and affordable financial services” that make the day-to-day lives of individuals and businesses easier. Having a bank account is considered to be the first step toward financial inclusion because transaction accounts allow people to store, send and receive payments.

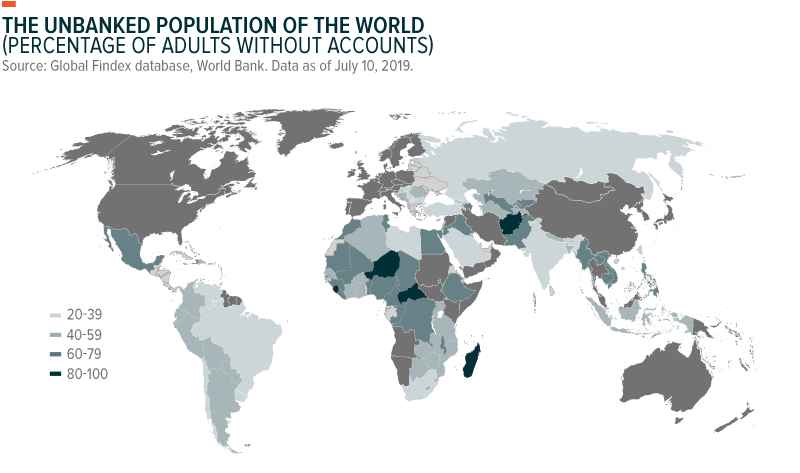

Today, 1.7 billion adults worldwide are unbanked, or do not have access to a bank account. Many unbanked people live in developing countries, which have a lack of infrastructure (i.e. electricity, internet access) and government regulation. There is a large unbanked population in the U.S., too, with “lack of funds” cited as the primary reason.

At the same time, financial inclusion is necessary for small and medium enterprises (SMEs): A high percentage of SMEs report limited access to credit as a key constraint, especially throughout the Middle East, North Africa and Central Asia regions.

If we look at the positive impact fintech has had on financial inclusion, two key examples stick out: the reduction of costs in payments and the increased access to credit for businesses in certain markets.

Furthermore, digital payment services are helping penetrate the financial inclusion landscape in more complex, rural landscapes, like India, which has seen a boost thanks to COVID-19. We will begin by highlighting some of the barriers to financial inclusion.

Historically, institutions have geared the sales of their services and products toward people who are likely to bring them a return. Taking a look back at how banks started we see that accounts were initially accessible only to the most economically active societal classes.

Over time, the percentage of people with access to financial services has gradually climbed. While access varies significantly from country to country, disparities in financial inclusion are evident.

Although many pilot programs have been implemented to boost microfinance, 6 percent of the unbanked population reside in Indonesia, with China and India holding the largest unbanked population. This is due to different fintech ecosystems, which are affected by infrastructure like the internet and electricity, government policies and the regulatory environment.

Quite surprising to many, a large number of the unbanked population reside in the U.S. While a lack of funds were cited as the primary cause, a lack of trust in financial institutions and privacy concerns were also popularly cited. Despite leading the world in fintech development, 19 percent of people in the U.S. have reported that their expenses exceed their income.

Further, Black and Hispanic communities in the U.S. comprise a large portion of the underbanked population. Despite the fact that this demographic spends around $200 billion in bank fees and interest rates to access financial services, Black and Brown Americans are at a clear economic disadvantage. Essentially, it is expensive being a minority in America.

The era of COVID-19 has caused huge shifts in the underbanked landscape. Digital services have propelled financial inclusion amid social distancing. Lockdown measures have resulted in a hike in fintech adoption—people are moving toward cashless options and businesses are discovering the benefits of bank payments as part of a global effort to mitigate the virus.

In other parts of the world, such as Kenya, Ghana and Myanmar, governments have encouraged the use of fintech platforms by lowering costs and increasing transaction limits. Such developments are accelerating the move toward digital financial services and away from more traditional services. Today, fintech is significantly contributing toward financial inclusion in several ways, including the markets they impact.

In many emerging markets, a lack of access to credit severely limits business growth. To make matters worse, banks can be hesitant to lend to smaller enterprises. In the MENAPregion, around 32 percent of firms report access to credit as a major constraint (in comparison to the world average of 26 percent). In the CCA region, the figure is lower, about 18 percent.

Fintech allows for alternatives to traditional lending methods. New electronic platforms in countries like China and Kenya have emerged that have led to the incredible success of businesses scaling up. For example, Alipay, and afterwards Ant Financial, a mobile and online payment platform in China, provides credit facilities to SMEs on Alibaba. It does this by collecting data from vendors’ transactions on platforms such as Taoboa, a Chinese e-commerce website.

Importantly, this process provides a solution which was previously unavailable to SMEs that found it difficult to access credit. As a result, SMEs in China have been empowered in three key ways.

First, Ant Financial lowers information asymmetry between itself and borrowers. This enables the platform to provide credit to companies that cannot access it from traditional banks because of a scarcity of information available.

The company is particularly helpful for startups that haven’t acquired the positive record of business operations needed from banks. Ant Financial provides a solution by collecting information that helps produce more precise risk pricing, as it can tailor the financial terms to suit each individual firm based on its risk profile.

Second, the process allows Ant Financial to develop savings tools that pool spare money from Taobao and redirect it to firms that need it. And third, as an online platform, Ant Financial helps more rurally located merchants access relevant trade finance—a goal that would have been unthinkable prior to the widespread adoption of the internet.

Crucially, Ant Financial is a formal institution that offers virtual banking licences, meaning it is subject to strict regulations. This aspect represents a key difference between fintech companies and other informal financing firms that do not hold contractual obligations enforced through a codified legal system. Regulators, therefore, consider fintech credit to constitute a form of alternative financing of more stability and clarity.

The innovative thinking, dedication and efforts of Alipay and other fintech players have advanced the opportunities for both consumers and businesses. Along with more accessible credit for SMEs, fintech has contributed to financial inclusion through less-costly digital payment platforms.

Digital payments have helped strengthen the payments landscape in several countries like Kenya, and have expanded access to digital financial tools and services.

This has had a positive effect on people working abroad, including migrant workers. Before digital payment providers, migrant workers—and their families back home—were largely excluded from financial services. When migrant workers send some of their earnings to their home country, these transfers are referred to as migrant remittances.

In the past few years, remittances have grown rapidly and now account for the largest source of income for several developing countries. In 2015, these workers sent $500 billion home, representing a huge flow of funds internationally. However, IMF statistics show transaction costs for remittances are high, particularly for lower amounts.

Digital payment solutions, like U.K. fintech app TransferWise, provide low cost, convenient solutions to store and transfer money. In 2019, Gobind Singh Deo, the Communications and Multimedia Minister in Malaysia, praised TransferWise for helping to improve financial inclusion and support Malaysia’s economic growth. Gobind said,

“The development of efficient, secure and cost-effective payment systems, such as those provided by TransferWise, will not only offer customers greater choice, but will also help improve financial inclusion by providing access to affordable financial services for all economic sectors and segments of society, thereby supporting balanced economic growth.”

Additionally, digital payments have facilitated increased account use in major emerging economies. In China, 57 percent of account owners now make purchases online—roughly double the amount in 2014.

Fintech pioneers are significantly advancing financial inclusion in other countries, too. Vodafone launched its M-Pesa app, which enables people to send money quickly, instantly and securely to anyone with a mobile phone, in Kenya back in 2007.

Prior to its launch, less than 20 percent of Kenyans had access to any type of formal payment service. Since its introduction, M-Pesa has transformed the livelihoods and economic landscape of millions of Kenyans. Among rural households, studies note an income increase of between 5 percent and 30 percent since the adoption of M-Pesa.

A similar strategy has been adopted in Indonesia. The development of Digital Financial Services (DFS) utilizes the uptake in mobile phone infrastructure to provide financial services to millions of unbanked consumers. The IMF has even called DFS “a promising channel to overcome geographical barriers to financial inclusion.”

The advancement of digital payment services has had significantly positive benefits in the emerging markets of Kenya, China and Indonesia. Looking to the future, we can already see how digital payments are contributing to financial inclusion in more complex, rural regions, like those in India.

The financial landscape in India looks vastly different from that of other regions: There are roughly 50,000 very small community banks and credit unions spread across many rural areas. Anyone visiting these rural areas will quickly notice there are no ATMs, no debit cards and limited services. The banks themselves serve as merely a place for consumers to deposit and withdraw funds at a counter.

As a result of the limited services, Mandar Agashe, founder, and managing director of Sarvatra Technologies, decided to develop a solution. Agashe set about helping smaller banks hook into a digital payment infrastructure and bring more consumers into the mix.

After years of attempting to make India more digital, Agashe’s quest was boosted by that country’s demonetization, combined with its Unified Payments Interface (UPI). COVID-19 safety measures also helped elevate the project further when more Indian consumers were forced to stay at home, and thus, carry out more transactions online.

In the first half of October 2020, UPI logged an enormous 1 billion transactions, crossing upwards of 2 billion by month-end. All-in-all, digital services are gaining momentum and contributing to financial inclusion to a broad section of society.

As a whole, fintech is undeniably contributing to financial inclusion. It is successfully expanding financial services and tools to those living abroad, in poorer households and in underdeveloped regions, through low-cost digital payment services.

Fintech is also increasing access to credit for struggling businesses, which has a positive economic impact. When businesses grow, more jobs become available.

Increased mobile phone infrastructure throughout the globe also has aided the adoption of these services, and has set the scene for more opportunities for financial services to naturally emerge.

Digital payments, the most advanced service, is expected to exceed $1 trillion in transaction value by 2025. Investment, lending and insurance services are surfacing on top of digital payments, with each skyrocketing by over 20 percent per year through to 2025.

While digital finance alone can’t fully close the gaps on financial inclusion, it is expected that the acceleration of e-payments could boost gross domestic product in markets such as the Philippines and Indonesia by 2 percent to 3 percent, and in Cambodia by 6 percent. When considering average wages, this would equate to a 10 percent rise in income in Indonesia, and a 30percent increase in Cambodia.

Recognizing the potential of digital finance could help create a promising future for financial services, especially in smaller markets such as Myanmar and Cambodia. Right now, just a small amount of the existing need for financial services are met by formal providers.

The development and expansion of digital financial services through advanced technologies will create unlimited possibilities for growth. This growth will not only apply to fintech or economies, but to the quality of life for those who have endured the hardships of experiencing financial exclusion.

Kiara Taylor is an expert on the integration of finance and technology. She writes about the impact of both micro and macro trends on global finance.

.webp)

.webp)