Fintech startups are hot in the Latin American venture capital market, with Fintech startups receiving over 50% of yearly investment dollars across the region. Nubank, Ualá, Geru, and Konfio are among Latin American fintech startups that raised significant rounds from international investors, including Tencent, Goldman Sachs, Morgan Stanley, and Vostok Emerging Finance in 2018. Two Brazilian fintech companies, PagSeguro and Stone Co, IPO’d in 2018 for more than $1B each.

The market opportunity for fintech in Latin America is big enough to accommodate these growing startups. Across the region, over 40% of the population is still unbanked, and millions of small businesses lack the capital they need to grow. Latin America also needs solutions for pressing issues like bill pay, online payments, and access to credit, processes that are notoriously complex and exclusionary across the region.

By comparison, the US market looks very different. While banks may not be the perfect solution to financial inclusion, only a tiny percentage of the US population could be considered unbanked. Up to 92% of US households have an account with` at least one formal financial institution. Most people have credit or debit cards and are comfortable with online transactions. Most individuals complete both directly through retailers’ sites and using payment platforms such as PayPal and Square.

5 lessons fintech companies can learn from Latin America

Within the US banking industry, there is enough competition to push banks to be relatively consumer-friendly. This is in stark comparison to the bureaucratic and exclusionary institutions that plague Latin American banking.

However, both regions are home to thousands of fintech startups seeking to disrupt the current system. These companies are working to provide better financial services for consumers. Despite significant differences in the two markets, US fintech startups would be wise to look to their Latin American counterparts to learn how to grow and consolidate within a rapidly-changing ecosystem.

Photo credit: Crunchbase News

Here are five lessons fintech startups can learn from Latin America.

1. Leapfrog over legacy technologies.

While 92% of bank customers in the US use online banking through their desktop, most Latin Americans access the Internet through their smartphones. By 2020, mobile Internet traffic in Latin America will be 55x more than total Latin American Internet traffic in 2005. In the US and Latin America, millennial and Gen Z customers will expect constant access to their banking services via smartphone.

Latin Americans are rapidly turning to mobile neobanks as an alternative to the exclusionary local banking system. Neobanks Nubank, Ualá, and albo raised a total of $320M, $50M+, and $8M respectively in 2018 to continue improving mobile banking and payments services in Latin America. Like Asia, Latin America has been able to adopt newer technologies more quickly than developed markets because few people had bank accounts in the first place.

While US fintechs must work around strong legacy systems, there is still opportunity to solve problems where current technologies leave gaps. Customers can be much quicker to adopt technology if it doesn’t require them to invest a lot of time and energy into shifting over from an older model. Mobile money in Latin America, Africa, and Asia has taken off much faster than in the US because many of those populations did not previously have access to finance. US startups should look ahead to create tech solutions that jump over existing systems, rather than simply modifying them.

2. Don’t underestimate the challenge of international markets.

Startups in the US have the advantage of a vast and diverse market where they can sell their products. Outside of Mexico and Brazil, growing startups in Latin America often struggle to become profitable while operating within just one country. Most countries in the region have fewer than 40 million people. In comparison, the US has a market of over 330 million people. For a Colombian startup (pop 50M) to reach a market the size of the US (330M), it would require establishing a presence in Mexico (130M), Argentina (44M), Peru (32M), Chile (18M), and Ecuador (16M).

This challenge means that Latin American startups often have a regional expansion plan to grow, which includes adapting to a new market and its regulations. For example, Ecuadorian Stripe clone Kushki Pagos expanded to Colombia using partnerships with local brands that help provide visibility and validation for their product. Kushki’s goal is eventually to integrate their product into banks, as they have done in Ecuador, but first they plan to achieve widespread acceptance by Colombian clients as a safe payment method.

By comparison, PayPal’s first forays into the Colombian market were clumsy at best. In 2015, the payments company withdrew from Colombia, making it impossible for customers to complete transactions in Colombian pesos. Only in late-2018 did PayPal make its way back into the market through a partnership with Colombian neobank, Nequi.

Local partners are often the key to a successful expansion strategy, especially for a complicated fintech product. Latin American fintech startups often include these partnerships in early growth plans, since expansion is essential to success in the regional market. US startups looking abroad should prepare to find local partners who can help manage cultural changes, make introductions, and provide validation for the brand in a new market.

3. Use local resources.

While the IRS in the US has only recently gotten on board with online tax returns and payments, Chile and Colombia have been filing taxes online for years. Chile specifically made electronic invoicing a legal requirement in 2004. This means every company in Chile files their monthly taxes online through a standardized format.

These invoices, submitted to the central government in XML format, mean the tax collection agency SII (Servicio de Impuestos Internos) has access to a lot of data. This unique circumstance created an opportunity for OmniBnk (previously Portal Finance) to create a financing scheme that used that data as an alternative credit score to provide faster and fairer interest rates to small businesses looking for short-term loans. This system is possible anywhere companies submit electronic invoices. So in places with fully online payment systems, like China, loans can be calculated automatically – with no bank involved.

Each country has its own financial regulations and systems that fintech startups must manage to grow. Latin American fintech startups in particular are known for coming up with wily solutions. These solutions leverage local resources to create simple and elegant financial solutions for their customers.

US fintech companies should take a page from Latin American fintech companies’ rulebook. They should look to use current LatAm systems to further simplify finances in their local markets.

4. Solve real pain points.

Many countries in Latin America still struggle with corruption, secure payments, low financial inclusion, and fraud. Banks and government institutions across the region are looking to technology to solve these entrenched problems. In particular, Brazil, Mexico, Argentina, and Chile are using blockchain technology to develop better contracts, safer bank transactions, and more transparent government spending.

For example, Brazil’s Creditas bypassed the struggling Brazilian credit rating system to create their own technology that provides secured customer loans without the bank. In a country where just 68% of people have an account at a formal financial institution, companies like Creditas solve pain points without resorting to traditional systems. Using its proprietary lending technology, Creditas has quickly grown to become one of Brazil’s most prominent fintech startups.

In Asia and Latin America, these institutions are “leapfrogging” over older legacy technologies. They are working to adapt to a rapidly-evolving global standard of transparency. While the pain points in the US may not be as obvious as in Latin America, they are still there. US startups might have to dig deeper to find an entrenched problem that needs solving. However, they should remember to only build a product or service that solves a pressing need. Latin American fintech startups that can’t solve a problem and sell fast will die quickly. US startups should follow the same mindset; market fit is the key to long-term growth.

Keeping an eye on Latin America

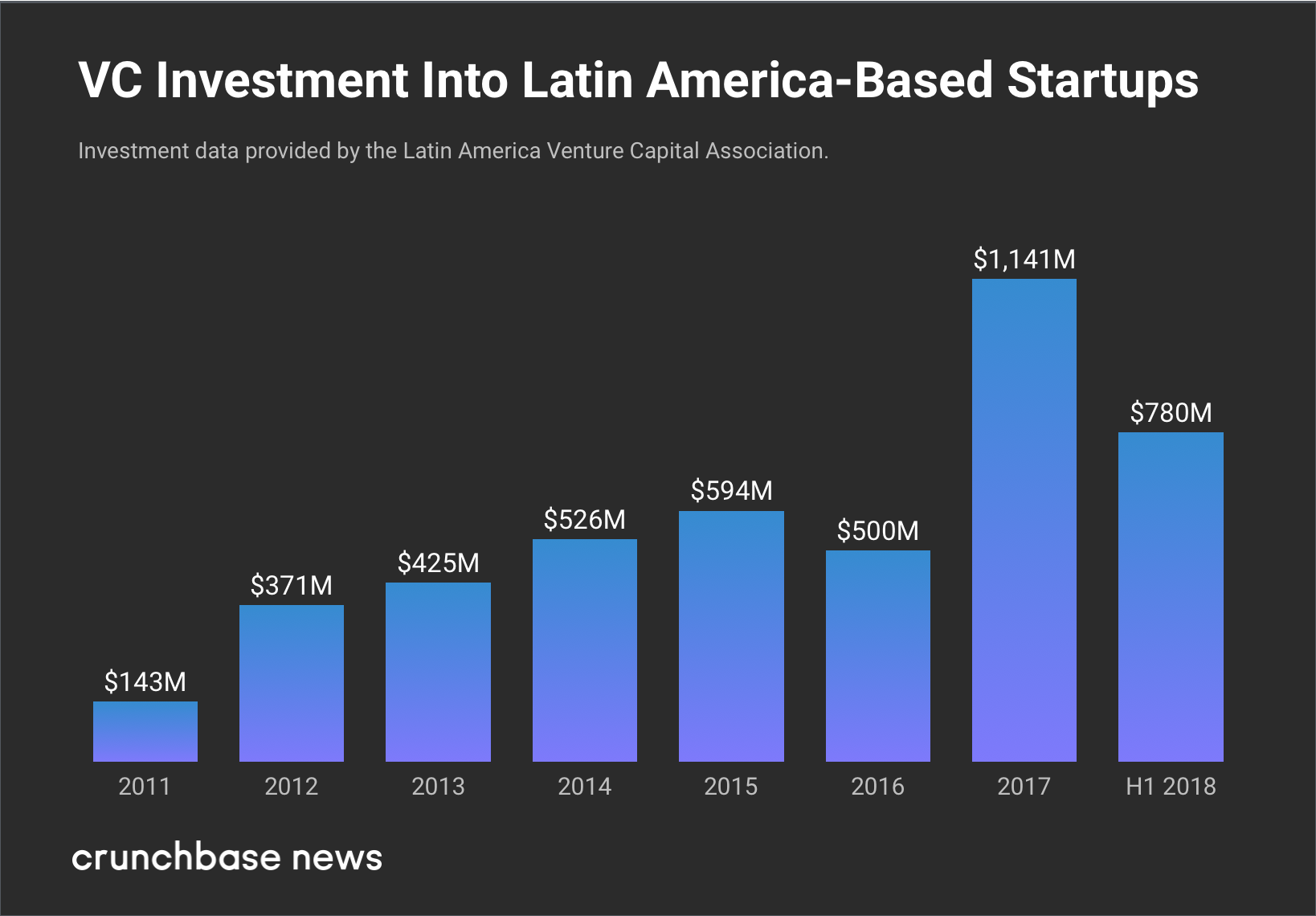

Financial technology is one of the most heavily-funded industries in the US and Latin America. Over half of the $1B invested in Latin American startups in 2017 went to fintech companies. In 2018, 25% of deals went to fintech startups. However, successful scaling looks very different for startups in Latin America and the US. There are many lessons US fintech companies can learn from Latin American startups’ scrappiness. Fostering strategic partnerships can help move their businesses forward.

Fintech companies in Latin America plan for international expansion. They focus on a population with access to smartphones, but not to banks. This discrepancy has often caused Latin American banks to partner with fintech startups. This trend is not as widespread in the US due to market saturation and regulations. In many cases, banks in the US prefer to pursue M&A agreements to access new technology, rather than startup partnerships.

However, the partnerships between Latin American banks and startups, including Ualá’s work with Banco Industrial de Argentina and Credicorp’s investment in Culqi, are worth watching and could be interesting models for banks and startups to replicate in other parts of the world as well.

By Nathan Lustig, entrepreneur and Managing Partner at Magma Partners, a seed stage investment fund with offices in Latin America, the US, and China. Follow him @nathanlustig